and Large Language Models (LLMs) Dangerous Future in 2025")

Starting a startup is an exhilarating journey filled with challenges, learning experiences, and the potential for great rewards. In recent years, the startup ecosystem has gained tremendous momentum, fueled by innovation and the relentless pursuit of solving real-world problems. Organizations like Y Combinator have played a pivotal role in nurturing budding entrepreneurs, providing them with the resources and mentorship needed to succeed. This article will explore the essential steps to start a startup, the importance of mentorship, and how to navigate the complexities of launching your own business.

Understanding the Startup Landscape

Before diving into the specifics of how to start a startup, it’s crucial to understand the landscape. The startup ecosystem comprises various players, including entrepreneurs, investors, mentors, and accelerators. Y Combinator, one of the most renowned startup accelerators, has been instrumental in shaping this ecosystem by providing early-stage startups with funding, guidance, and networking opportunities.

The Role of Y Combinator

Y Combinator has funded over 2,000 startups, including well-known companies like Airbnb, Dropbox, and Reddit. Their model emphasizes the importance of mentorship and community support, which is vital for new entrepreneurs. By participating in Y Combinator’s program, founders gain access to a wealth of knowledge and experience that can significantly increase their chances of success.

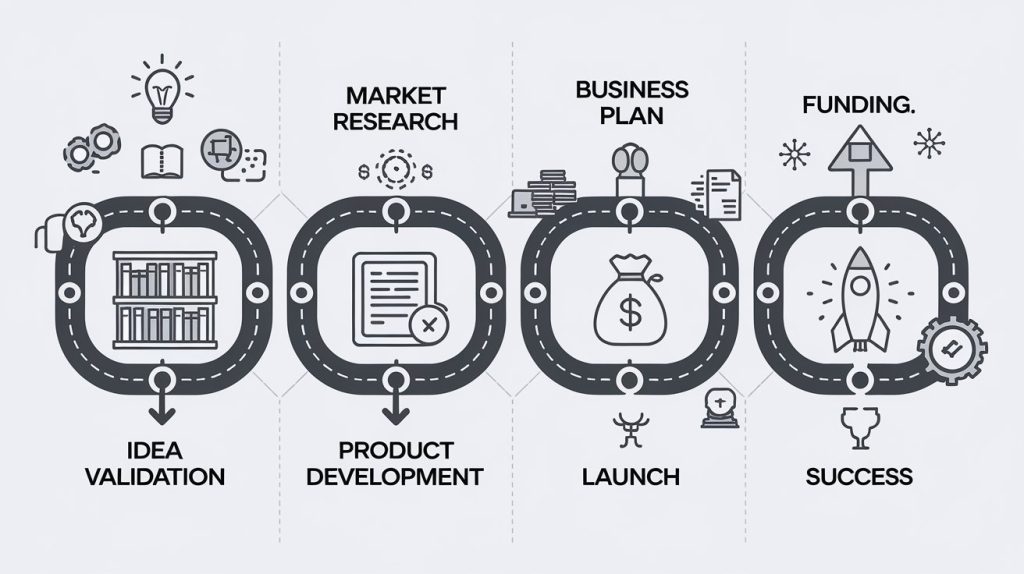

Step 1: Identify a Problem to Solve

The first step in starting a startup is identifying a problem that needs solving. Successful startups often emerge from the founder’s personal experiences or frustrations. Ask yourself:

- What challenges do I face in my daily life?

- Are there inefficiencies in existing solutions?

- How can I leverage my skills and expertise to address these issues?

By pinpointing a specific problem, you can develop a solution that resonates with potential customers.

Step 2: Validate Your Idea

Once you’ve identified a problem, it’s essential to validate your idea before investing significant time and resources. This can involve:

- Conducting market research to understand your target audience.

- Gathering feedback from potential users through surveys or interviews.

- Creating a minimum viable product (MVP) to test your concept in the market.

Validation is crucial because it helps you determine whether your solution has a genuine demand and if it’s worth pursuing further.

Step 3: Build a Strong Team

A successful startup is rarely a solo endeavor. Building a strong team is critical to your startup’s success. Look for co-founders or early team members who complement your skills and share your vision. Consider the following attributes when assembling your team:

- Expertise in relevant fields (e.g., technology, marketing, finance).

- A shared passion for the problem you’re solving.

- A willingness to adapt and learn in a fast-paced environment.

Having a diverse and skilled team can significantly enhance your startup’s chances of success.

Step 4: Develop a Business Plan

A well-thought-out business plan serves as a roadmap for your startup. It should outline your business model, target market, marketing strategy, and financial projections. While plans can evolve over time, having a clear vision will help you stay focused and make informed decisions.

Incorporating Feedback

As you develop your business plan, consider seeking feedback from mentors and industry experts. Organizations like Y Combinator encourage entrepreneurs to iterate on their ideas based on constructive criticism. This iterative approach can lead to a more refined and viable business model.

Step 5: Secure Funding

Funding is often a significant hurdle for startups. There are various options available, including bootstrapping, angel investors, venture capital, and crowdfunding. Each option has its pros and cons, so it’s essential to choose the one that aligns with your startup’s goals and needs.

- Bootstrapping: Using personal savings or revenue generated from the business to fund operations.

- Angel Investors: Wealthy individuals who provide capital in exchange for equity.

- Venture Capital: Firms that invest in startups with high growth potential in exchange for equity.

- Crowdfunding: Raising small amounts of money from a large number of people, typically through online platforms.

The Y Combinator Advantage

Participating in a program like Y Combinator can provide not only funding but also invaluable mentorship and networking opportunities. Many successful startups credit Y Combinator for their initial funding and guidance, which helped them navigate the early stages of their business.

Step 6: Launch and Iterate

Once you’ve secured funding and developed your product, it’s time to launch. However, launching is just the beginning. Continuously gather feedback from users and iterate on your product to improve its features and address any issues. This agile approach is vital for adapting to market demands and ensuring long-term success.

Step 7: Focus on Growth

After launching your startup, focus on scaling your business. This can involve:

- Expanding your marketing efforts to reach a broader audience.

- Exploring new sales channels or partnerships.

- Continuously improving your product based on user feedback.

Y Combinator emphasizes the importance of growth and encourages startups to focus on metrics that matter. Understanding your key performance indicators (KPIs) will help you make data-driven decisions and drive your startup’s success.

Conclusion

Starting a startup is a challenging yet rewarding endeavor. By following these steps and leveraging resources like Y Combinator, aspiring entrepreneurs can increase their chances of success. The journey may be filled with obstacles, but with determination, a solid team, and a focus on solving real problems, anyone can turn their startup dreams into reality.

Also Read How to get funding for your startup

Youtube Video Ycombinator Should you start a startup